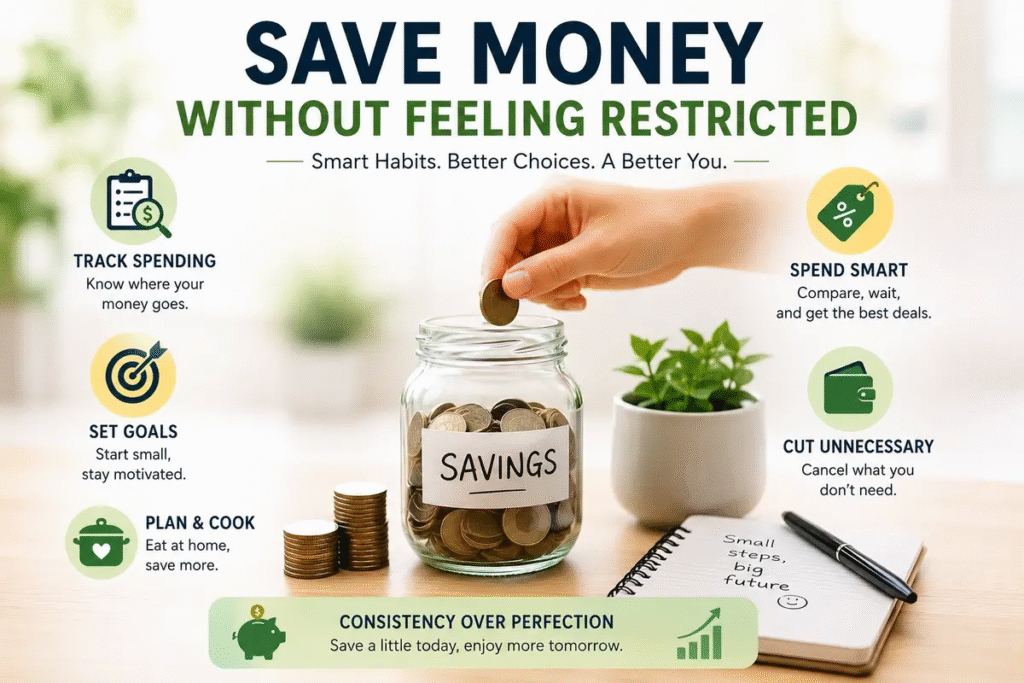

Let’s be completely honest about the personal finance world: most money-saving advice feels like it was written by someone who deeply despises fun. You open an essay looking for a way to build a modest financial safety net, and within three paragraphs, you’re told to brew lukewarm coffee at home until the day you die, cancel every streaming service you actually use, and spend your weekends staring at a blank wall to save on your electric bill. It’s exhausting, it’s depressing, and quite frankly, it never actually works long-term.

When you treat saving money like a crash diet of pure self-denial, you set yourself up for the exact same result: a brief window of intense misery followed by an explosive impulse-buying spree because you simply couldn’t take it anymore.

The secret to building a functioning bank account that doesn’t completely evaporate every three months isn’t extreme frugality. It is intentional alignment. It’s about realizing that money is just an energy exchange, and right now, a lot of your funds are probably leaking out into things you don’t even actually care about. When you learn how to plug those silent leaks, you suddenly find yourself with extra cash without ever feeling like your daily life got smaller.

The Fatigue of the Frictionless Purchase

For most of us, the problem isn’t that we’re buying too many luxury sports cars or high-end designer watches. The problem is that spending has become entirely friction-free, deeply automatic, and heavily tied to our emotional states. We live in a modern marketplace engineered specifically to separate you from your cash with a single thumb-scan, facial recognition check, or one-click buy button.

Think about how incredibly easy it is to justify an expensive food delivery order on a Thursday night because you had a brutal day at the office. You don’t even particularly want that specific food—it often arrives lukewarm and slightly soggy—but you desperately wanted the sweet relief of not having to make another decision. That isn’t spending money to support a luxury lifestyle; that is spending money to temporarily patch an emotional leak.

When you look at your bank accounts through a real human lens rather than a rigid mathematical ledger, you start to see that saving cash isn’t about cutting out the milestones that keep you happy. It’s about stopping the unconscious hemorrhage of funds on convenience items that give you absolutely nothing in return.

Establishing Your Personal Joy-to-Cost Balance

If you want to save cash without feeling like you’re constantly punishing yourself, you need to establish your own personal balance of joy versus cost. Every single dollar that leaves your pocket should be evaluated based on how much genuine, lasting utility or genuine comfort it brings into your world.

The Value Rule: High Joy / Low Cost is an absolute win. High Joy / High Cost requires deep planning. Low Joy / High Cost is simple financial sabotage.

Everyone’s life priorities look vastly different because everyone values different elements of daily existence. Consider how much two distinct people might vary:

If your favorite part of the week is sitting down at a specific local diner with your friends on Saturday morning, do not cut that out of your life. That breakfast is keeping you sane. Instead, point your scissors toward the areas you don’t actually care about. Maybe you’re paying a massive monthly fee for a luxury gym subscription you haven’t stepped inside since the new year started, or your car insurance premium has quietly crept up over the last two years because you haven’t checked for a competitor’s rate. Redirecting cash away from that dead weight leaves your true joy fully intact.

Designing a Dynamic Budget That Doesn’t Induce Tears

The word “budget” has honestly terrible branding. It sounds like a financial straightjacket designed to keep you from doing anything remotely interesting. But a real budget isn’t a prison sentence; it’s simply a clear roadmap that tells your money where to go so you don’t have to spend your life wondering where it went.

If your financial plan is too rigid, you will abandon it within a fortnight. That is why flexible frameworks work best for real human beings.

The Simple Three-Bucket Approach

Instead of tracking every single copper coin into thirty different microscopic categories (which is a fast track to mental burnout), try dividing your net income into three clean, unmistakable areas:

- The Foundations: This is the non-negotiable stuff. Rent or mortgage payments, basic utilities, everyday groceries, insurance, and minimum debt payments. If this area is consistently taking up nearly all your income, it’s a sign that your fixed living costs are too high for your current setup, no matter how many lattes you cut out.

- The Future: This money goes directly into savings, long-term investments, or aggressive principal debt payoffs the absolute moment your paycheck hits your account. You don’t look at it, you don’t negotiate with it, and you don’t use it to buy casual shoes.

- The Guilt-Free Fun: This is your psychological pressure valve. Event tickets, fancy cheeses, vintage clothing, or random tech gadgets. Once the first two buckets are safely taken care of, you are allowed—and explicitly encouraged—to spend this cash down to absolute zero with zero guilt.

The Art of the Invisible Cut

The absolute easiest way to stack cash without changing your day-to-day experience is to execute what is known as an invisible cut. These are adjustments that take place entirely behind the scenes, targeting the silent drains on your bank account that provide zero actual lifestyle value.

Take a single afternoon to download your last few bank statements, sit down with a warm drink, and look for the “zombie charges.” We all have them: a streaming service you signed up for to watch one trending documentary six months ago, a premium storage app you don’t use, or an auto-ship supplement delivery that is currently stacking up unopened in your hallway closet.

Trimming these out doesn’t make your life feel smaller. You aren’t losing a genuine experience; you’re simply stopping a distant corporation from quietly siphoning off your hard-earned cash while you sleep.

Deconstructing the Impulse Trigger Before It Happens

Most impulsive spending doesn’t happen because we actually want the item in question; it happens because we are desperately trying to transition from one emotional state to another. We buy things when we are bored, lonely, physically exhausted, or feeling temporarily inadequate.

To protect your savings without feeling restricted, you need to introduce a conscious buffer between the initial impulse and the final transaction.

The next time you see something online that you suddenly feel you absolutely must own, implement a multi-day waiting period. Put the item in your shopping cart, close the internet browser tab, and walk entirely away for three full days.

If, after the waiting period, you are still actively thinking about that item and can clearly articulate how it will genuinely improve your daily life, go ahead and buy it with a clear conscience. But more than half the time, you’ll realize you completely forgot it even existed. The urge wasn’t about the object; it was just a passing cloud of weekday boredom that has now drifted away, leaving your funds safely inside your account.

Upgrading Your Weekly Routine with Creative Alternatives

Living an exceptionally good life doesn’t require spending a massive fortune; it just requires a bit of tactical creativity. A lot of the things we spend massive amounts of money on can be easily swapped for alternative options that feel just as premium but cost a fraction of the price.

| The High-Cost Habit | The Smart Alternative | Why It Feels Just as Good |

|---|---|---|

| Overpriced, noisy restaurant dates | A curated aesthetic picnic in a quiet park | More intimate, better conversation, custom menu |

| Commercial cinema tickets + snacks | A themed home movie night with a projector | Zero crowds, actual comfort, pause button privilege |

| Massive, expensive vacation travel | A highly specific, targeted regional road trip | Less airport stress, discovery of hidden local gems |

Look closely at your social habits. If you love hosting the people you care about, you don’t need to cater an expensive meal from a premium restaurant to create a memorable evening. A well-organized potluck or a casual night focused on simple board games and homemade pizzas often leaves people feeling far more connected and relaxed than a stiff, expensive dinner at a crowded downtown establishment. It’s about prioritizing the deep human connection over the high price tag.

Building a Low-Pressure Safety Net

The ultimate luxury that money can buy isn’t a designer handbag or a luxury vehicle; it is breathing room. The feeling of knowing that if your car’s alternator explodes on a Tuesday morning, or if your landlord suddenly raises your monthly utilities, your life isn’t going to fall completely apart. That sense of baseline security is the ultimate lifestyle upgrade.

You do not need to build a massive six-month emergency fund in a single weekend. Thinking you need thousands of dollars saved immediately is exactly what keeps people from starting at all.

When the money moves automatically before you ever see it hit your primary checking account, your brain naturally adjusts its spending baseline to whatever is left over. You don’t feel the loss of that small transfer because you never gave yourself the chance to consider it spending money in the first place. Over a year, those quiet, automatic movements compound into a real financial shield that protects your peace of mind every single day.

Prioritizing Intention Over Deprivation

At the end of the day, managing your personal finances successfully comes down to a fundamental shift in your internal perspective. Saving money shouldn’t feel like a constant, agonizing battle against your own desires. It should feel like a deep act of self-respect.

When you say no to a thoughtless, low-value purchase, you aren’t depriving yourself of a treat. You are actively saying yes to a future version of yourself that is less stressed, more secure, and completely in control of their own destiny. You are choosing to trade a brief, fleeting moment of consumer convenience for long-term freedom and confidence. By automating the dry parts of your finances, ruthlessly cutting the things that don’t matter, and fiercely protecting the spending that genuinely enriches your life, you build a sustainable lifestyle. You get to live exceptionally well today, while quietly building a beautiful foundation for tomorrow.

FAQs

1.How can I save money without feeling deprived?

The best way to save money without feeling deprived is to focus on what truly matters to you and cut back on the things that do not add much value. When your spending reflects your priorities, saving feels more natural. It also helps to keep room in your budget for small pleasures so your lifestyle still feels enjoyable.

2.What is the easiest way to start saving money?

A simple way to begin is by tracking your spending for a month and identifying where your money is going. From there, you can make small changes like reducing unused subscriptions, planning meals, or setting up automatic transfers into savings. Starting small makes the process feel less overwhelming.

3.Do I need a strict budget to save money?

No, a strict budget is not necessary. In fact, many people do better with a flexible budget that still allows for fun and comfort. The most important thing is knowing your income, your regular expenses, and the areas where you can save without making life feel restrictive.

How much should I save each month?

The right amount depends on your income, expenses, and goals. Some people start with a very small amount, while others can save more. What matters most is consistency. Even saving a little each month can build strong habits and create meaningful progress over time.